Last Friday marked the conclusion of a two-week period during which the benchmark indexes maintained their previous level of stability. After getting off to a strong start, the indexes spent the rest of the week trading inside a range, following mixed indications from across the world. The mood of the market shifted, however, as a result of a significant recovery in the last session.

The Sensex finished the week at 62,501.69, while the Nifty was able to break over the barrier located at 18,400 and settle at the high point of the week, which was recorded at 18,499.35. The recovery was helped along by contributions from every industry, with the metal, pharmaceutical, and information technology sectors leading the pack.

Earnings reports are expected to remain front and centre for the next week, particularly in the small and midcap segments of the market, where over 1,700 businesses are expected to declare their quarterly figures. From a macroeconomic point of view, the market movement will be guided by the statistics on auto sales, the GDP growth rate, and the PMI.

The behaviour of markets in the United States after the White House and Republicans achieved an agreement to raise the debt limit and prevent an impending default will also be a significant guiding factor for markets in most other countries across the globe.

“The Nifty looks set for a new high after the consolidation breakout, thanks to improved participation from across sectors,” said Ajit Mishra, VP Research, Religare Broking. “Though we are seeing broad-based buying, the focus should remain on identifying the leaders from the respective sectors instead of adding laggards in the hope of recovery.”

Here are ten of the most important elements that will keep traders busy throughout the next week:

1) Corporate Earnings

As we reach the last week of earnings season, nearly 1,700 firms are scheduled to publish their quarterly figures by June 4, which is the deadline for this year’s earnings season. The vast majority of these businesses belong to the small-cap market; however, there are also some well-known corporations like IRCTC, Apollo Hospitals, and Adani Ports on the waiting list.

The figures for the March quarter have not yet been categorised. The majority of software companies have let Wall Street down, as have industries focused on exporting in the face of a decline in demand from Western countries. However, there have been some unexpected developments, most notably in the financial sector.

2) Auto sales data

Traders will keep a close watch on the monthly vehicle sales figures for May, which businesses will begin disclosing beginning on June 1. Since the beginning of the past couple of months, the sales volume of automobiles manufactured in India has increased only slightly in the local market, while it has remained stagnant on the export market.

Traders will thus pay attention to any signs of improvement in the sales figures for the month of May.

3) GDP data

The figures about India’s gross domestic product (GDP) growth for the quarter and the year that ended in March will be released the following week. The general prognosis for the Indian economy is expected to improve as a result of several experts’ projections that India’s GDP growth in FY23 will exceed the formerly estimated rate of 7 percent.

If this occurs, we might see a bullish reaction from the market.

4) US debt limit

An impasse that has lasted for many months has been broken as US Vice President Joe Biden and senior Republican in Congress Kevin McCarthy came to a preliminary agreement on how to raise the debt limit from its current level of $31.4 trillion.

The agreement would assist the United States in avoiding an economically destabilising default, provided that it is successfully passed through Congress, which is currently deeply divided, before the Treasury Department runs out of money to cover all of its obligations, which the department warned would happen if the debt ceiling is not raised by June 5; the warning came on Friday.

It would be a significant setback for the market if the transaction was not successful in its completion.

5) PMI data, infrastructure output

The statistics from the manufacturing Purchasing Managers’ Index (PMI), which will provide insight on the demand condition at plant levels in May, will also be monitored by market players. It is anticipated that the PMSI will come in on the positive side but that it will likely be lower than the reading from the prior month.

On May 31, India will announce statistics regarding the production of its infrastructure for the month of April. On June 2, India will reveal data regarding their foreign currency reserves for the week ending May 26, as well as bank loan and deposit growth for the week ending May 19.

6) FII Flow

This month, international investors have been optimistic about the Indian market, which has helped improve the atmosphere on Dalal Street. They have made equity purchases of Rs 37,317 crore so far throughout the month of May. Over the course of the most recent three months, outside investors have been net buyers of shares.

7) Technical View

When taking into account the consolidation breakout with considerable rallies on the previous Friday, the Nifty50 seems to be inching towards its next goal of roughly 18,700 levels. If it is able to clear this target, the door may open for a record high of 18,887 on December 1, with key support around 18,400–18,200 levels, according to the opinions of industry analysts.

According to observations made by Subash Gangandharan, Senior Technical and Derivative Analyst at HDFC Securities, the Nifty has broken above the previous swing high of 18459, suggesting that bulls continue to maintain control of the market on the daily chart.

“We anticipate that the upward trend will continue in the sessions to come. The Nifty currently has immediate upside goals located at 18,696. There is still the possibility of corrective action in the near future. Important supports to keep an eye on for signs of weakening are located at 18,333,” he stated.

Gangandharan continued by saying that as a result of the bulls’ return, the near-term trend of the Nifty remains upwards, and it is possible that the index will continue to go higher until the immediate resistance level of 18509 is broken. 18 696 should be the immediate goal.

8) F&O cues, India VIX

On the upper side, the weekly option data revealed that 18,700–19,000 are projected to be important barriers for the Nifty, with the essential support region being located between 18,400–18,200.

The largest amount of open interest in calls was noted at the 19,000 strike, followed by the 18,700 and 18,500 strikes, with considerable call writing occurring at the 18,700, 18,800, and 19,000 strikes.

On the put side, the 18,300 strike has the most open interest, followed by the 18,400 and 18,200 strikes, with writing taking place at the 18,400 strike, the 18,300 strike, and the 18,500 strike.

Bulls received further support from reducing volatility for the second trading day in a row. The India VIX, which gauges the predicted volatility in the next thirty days for the Nifty, decreased by 9.2 percent over the course of the previous two days, falling from 13.11 levels to 11.90 levels. During the course of the week, it fell by 3.3 percent.

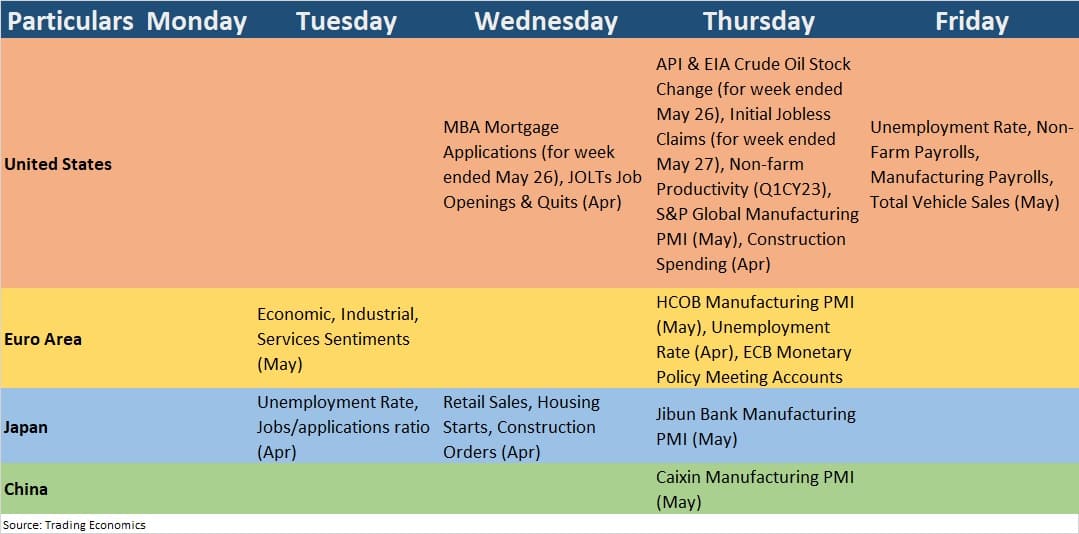

9) Global Economic Data Points

Here are key global economic data points to watch out for next week:

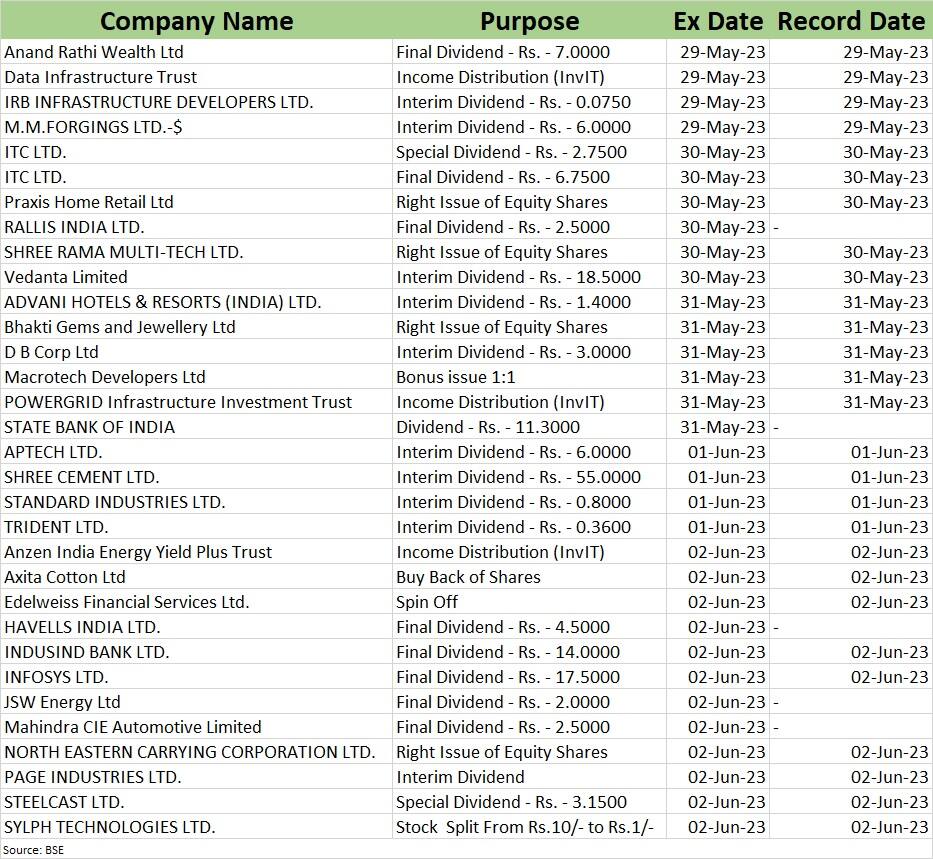

10) Corporate Action

The following companies’ stocks will stop paying dividends the next week: ITC, Vedanta, State Bank of India, Shree Cement, IRB Infrastructure Developers, Anand Rathi Wealth, Rallis India, DB Corp., Trident, Havells India, JSW Energy, Mahindra CIE Automotive, and Page Industries.

Here are key corporate actions taking place in coming week: